Futures Market: Overnight, LME copper opened at $9,640/mt, dipping to a low of $9,603.5/mt shortly after the opening bell. It then fluctuated considerably upward, reaching a high of $9,660/mt near the close, and ultimately settled at $9,649/mt, up 0.11%. Trading volume reached 14,000 lots, and open interest stood at 284,000 lots. Overnight, the most-traded SHFE copper 2507 contract opened at 78,050 yuan/mt, fluctuating upward to a high of 78,220 yuan/mt during the session, before fluctuating downward to a low of 77,960 yuan/mt. It rebounded slightly near the close, ultimately settling at 78,140 yuan/mt, down 0.08%. Trading volume reached 26,000 lots, and open interest stood at 191,000 lots.

[SMM Copper Morning Meeting Summary] News: (1) According to a recently approved maintenance plan, First Quantum Minerals will spend approximately $20 million per month to maintain its idle Cobre Panamá copper mine. Roderick Gutiérrez, President of the Panamanian Chamber of Mines, stated that costs would be covered by selling copper concentrates stored at the mine. The company currently holds 121,000 mt of concentrates, although some have degraded after nearly two years of idleness. Gutiérrez noted in an interview with local media that reprocessing these degraded materials may not be economically feasible.

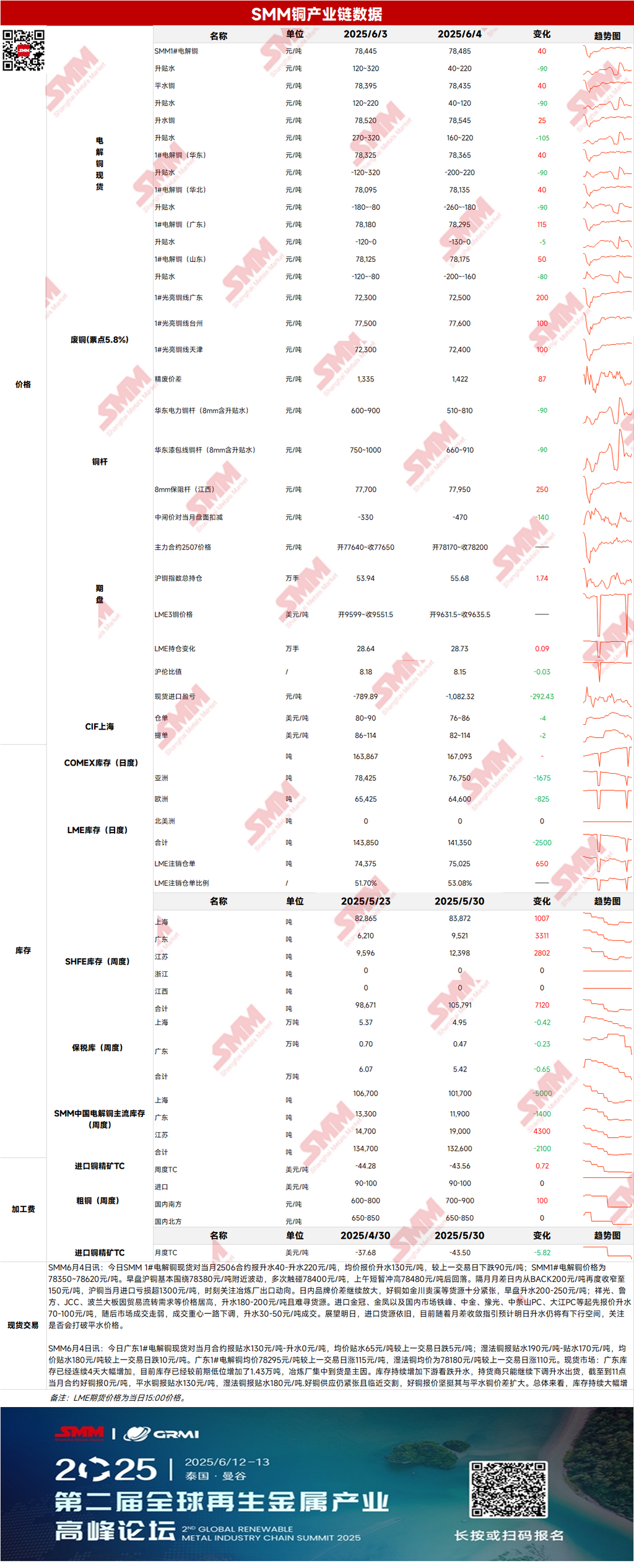

Spot: (1) Shanghai: On June 4, SMM #1 copper cathode spot prices against the front-month 2506 contract were quoted at a premium of 40-220 yuan/mt, with an average premium of 130 yuan/mt, down 90 yuan/mt from the previous trading day. The SMM #1 copper cathode price range was 78,350-78,620 yuan/mt. In the morning session, SHFE copper primarily fluctuated around 78,380 yuan/mt, touching 78,400 yuan/mt multiple times, and briefly surging to 78,480 yuan/mt before pulling back. The price spread between futures contracts (BACK) narrowed from 200 yuan/mt to 150 yuan/mt during the day. The import loss for front-month SHFE copper exceeded 1,300 yuan/mt. Close attention should be paid to smelter export dynamics. Imported supply remains available. Given the current convergence of the price spread, there is expected to be downside room for premiums tomorrow, with attention on whether parity pricing will be breached.

(2) Guangdong: On June 4, Guangdong #1 copper cathode spot prices against the front-month contract were quoted at a discount of 130 yuan/mt to a premium of 0 yuan/mt, with an average discount of 65 yuan/mt, down 5 yuan/mt from the previous trading day. SX-EW copper was quoted at a discount of 190 yuan/mt to 170 yuan/mt, with an average discount of 180 yuan/mt, down 10 yuan/mt from the previous trading day. The average price of Guangdong #1 copper cathode was 78,295 yuan/mt, up 115 yuan/mt from the previous trading day, while the average price of SX-EW copper was 78,180 yuan/mt, up 110 yuan/mt. Overall, with inventory continuing to rise sharply, spot premiums have been declining, and overall trading activity has been moderate.

(3) Imported Copper: On June 4, warrant prices ranged from $76 to $86/mt, with a QP in June, and the average price fell $4/mt from the previous trading day. B/L prices ranged from $82 to $114/mt, with a QP in July, and the average price fell $2/mt from the previous trading day. EQ copper (CIF B/L) prices ranged from $38 to $54/mt, with a QP in July, and the average price fell $7/mt from the previous trading day. Quotations referenced cargoes expected to arrive in mid-to-late June. Overall, the market continued the trend from yesterday. Due to unfavorable SHFE/LME price ratios, buyer purchase willingness was weak. However, there remains bullish sentiment toward forward premiums, with some traders choosing to purchase on dips.

(4) Secondary Copper: On June 4, the price of secondary copper raw materials rose by 200 yuan/mt MoM. In Guangdong, the price of bare bright copper ranged from 72,400 to 72,600 yuan/mt, up 200 yuan/mt from the previous trading day. The price difference between copper cathode and copper scrap was 1,422 yuan/mt, increasing by 87 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 1,130 yuan/mt. According to the SMM survey, as various regions gradually strengthen the enforcement of "reverse invoicing," some secondary copper rod enterprises have reported that local tax authorities have suspended issuing VAT invoices for small and micro enterprises. As provinces and cities continue to promote this policy, future input tax credits for secondary copper rod enterprises will be dominated by "reverse invoicing."

(5) Inventory: On June 4, LME copper cathode inventory decreased by 2,500 mt to 141,350 mt. On the same day, SHFE warrant inventory increased by 529 mt to 31,933 mt.

Prices: On the macro front, the ADP National Employment Report released on Wednesday showed that private sector employment in the US increased by only 37,000 in May, far below expectations. Following the data release, Trump once again called on Fed Chairman Powell to lower interest rates. The US dollar index fell, returning to a six-week low, which is bullish for copper prices. On the fundamental front, from the supply side, there is a severe shortage of mainstream high-quality copper supply. Suppliers, due to the tight supply, have extremely low willingness to sell at low prices. Looking ahead today, with the guidance of narrowing price spreads between futures contracts, it is expected that there will still be downside room for premiums. Attention should be paid to whether the parity price will be broken. In terms of prices, with ongoing tariff concerns, it is expected that there will be limited upside potential for copper prices today.

[The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make prudent decisions and should not rely on this as a substitute for independent judgment. Any decisions made by clients are not related to SMM.]